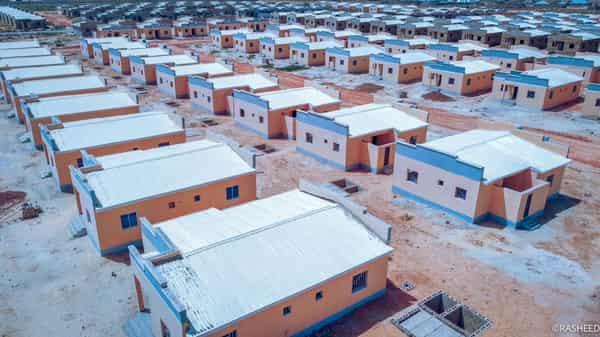

Nigeria’s real estate sector entered 2025 with strong optimism, driven by rapid urbanisation, renewed infrastructure investment and rising demand for housing across major cities.

However, as the year unfolded, chronic funding shortages emerged as the defining challenge, reshaping the pace, structure and outcomes of property development nationwide.

Despite sustained demand from a growing population and expanding urban centres, access to affordable capital remained a major constraint for developers and investors.

High interest rates, delayed mortgage disbursements and limited long-term financing slowed construction activities, stalled projects and forced many developers to scale back ambitious plans.

Medium- and large-scale developers, in particular, struggled to balance rising costs with tightening credit conditions, eroding profitability and dampening investor confidence.

The funding squeeze was worsened by sharp increases in the cost of building materials. Inflation, import dependence and logistical bottlenecks pushed prices higher, significantly raising construction expenses. Industry estimates show that building materials account for between 30 and 50 per cent of total project costs and influence up to 80 per cent of construction timelines.

With most materials—aside from cement—imported, developers were exposed to exchange rate volatility and escalating landing costs, further straining budgets.

Private control of the building materials market also amplified price instability, as supply-and-demand pressures and the activities of middlemen drove up costs.

Experts argue that treating building materials purely as market commodities ignores housing’s status as a basic social need, calling for stronger government intervention to stabilise prices and improve local production capacity.

Location-related costs added another layer of complexity. Construction in peri-urban and rural areas proved significantly more expensive due to transportation challenges and limited proximity to manufacturing hubs.

This disparity discouraged development outside major cities, reinforcing congestion in urban centres and deepening regional housing inequalities.

The combined effect of limited funding and rising costs had far-reaching implications. Affordable housing projects suffered setbacks, project completion timelines were extended, and the risk of abandonment increased. In some cases, cost pressures encouraged the construction of substandard buildings, while rent prices surged as housing supply lagged behind demand.

Government interventions offered some relief but fell short of resolving structural financing challenges. While federal and state initiatives focused on affordable housing delivery, mortgage access remained uneven.

Stakeholders raised concerns about delays and bottlenecks in mortgage disbursement under existing schemes, warning that weak oversight could undermine long-term housing finance reforms.

Meanwhile, 2025 also witnessed a surge in demolitions, particularly in Lagos and parts of the Federal Capital Territory, further tightening housing supply.

The removal of allegedly illegal structures, combined with slow project delivery, intensified accommodation shortages and pushed property values higher in high-demand areas such as Lekki, Ikoyi, Victoria Island and prime districts in Abuja.

Yet, amid the constraints, the sector showed resilience and adaptation. Developers increasingly turned to technology, with smart home features and virtual property tours becoming more common, especially in upscale estates.

Mixed-use developments gained traction, while logistics hubs, data centres and residential properties continued to attract investment interest. Government efforts to digitise land registries and improve transparency also signalled gradual progress.

Industry leaders described 2025 as a transitional year—one marked by innovation and survival rather than rapid expansion.

While the sector continued to contribute significantly to employment and GDP, stakeholders agreed that sustainable growth hinges on improved access to long-term, low-cost financing, clearer land policies, stronger regulation and continued infrastructure investment.

As Nigeria looks ahead to 2026, experts believe that sustained reforms, better mortgage supervision and deliberate government intervention in land and infrastructure provision could help unlock institutional capital and restore confidence.

Until then, funding shortages will remain the central force that reshaped Nigeria’s property market in 2025, defining both its struggles and its cautious resilience.